Financial Focus - East Winds and European Strains

Published September 2025 in Distinctly Winkleigh

The summer months have been marked by a divergence in fortunes across global markets. Japan’s stock market has enjoyed a resurgence that carried the Nikkei 225 to multi-decade highs, a development that has attracted widespread international attention. At the same time, the major economies of continental Europe have faced more persistent difficulties, with both France and Germany contending with structural headwinds that continue to weigh on growth. In the United Kingdom, the policy debate has turned increasingly towards the forthcoming Autumn Budget, which arrives in the context of persistent inflation and careful manoeuvring from the Bank of England.

Japan’s recent strength owes much to a combination of domestic reforms and international flows. Corporate governance changes urged by the Tokyo Stock Exchange have drawn favourable notice, while a measured shift by the Bank of Japan away from its long-standing policy of ultra-low interest rates has reassured investors that liquidity will not be withdrawn too abruptly. Capital seeking diversification has also flowed into Tokyo, particularly as China’s economic outlook has cooled. The question now is whether the positive sentiment can translate into sustained domestic momentum, supported by wage growth and consumption, or whether it remains largely an externally driven rally.

Across the Channel, the picture has been more subdued. France continues to wrestle with political uncertainty and fiscal reform, with debt levels under scrutiny in Brussels and consumer sentiment fragile. Germany, traditionally Europe’s industrial powerhouse, has struggled with weak exports and a slowdown in manufacturing output. Energy costs remain a drag and the hoped-for rebound in industry has yet to materialise. Taken together, these challenges illustrate the pressures facing the eurozone at a time when broader global growth is also moderating.

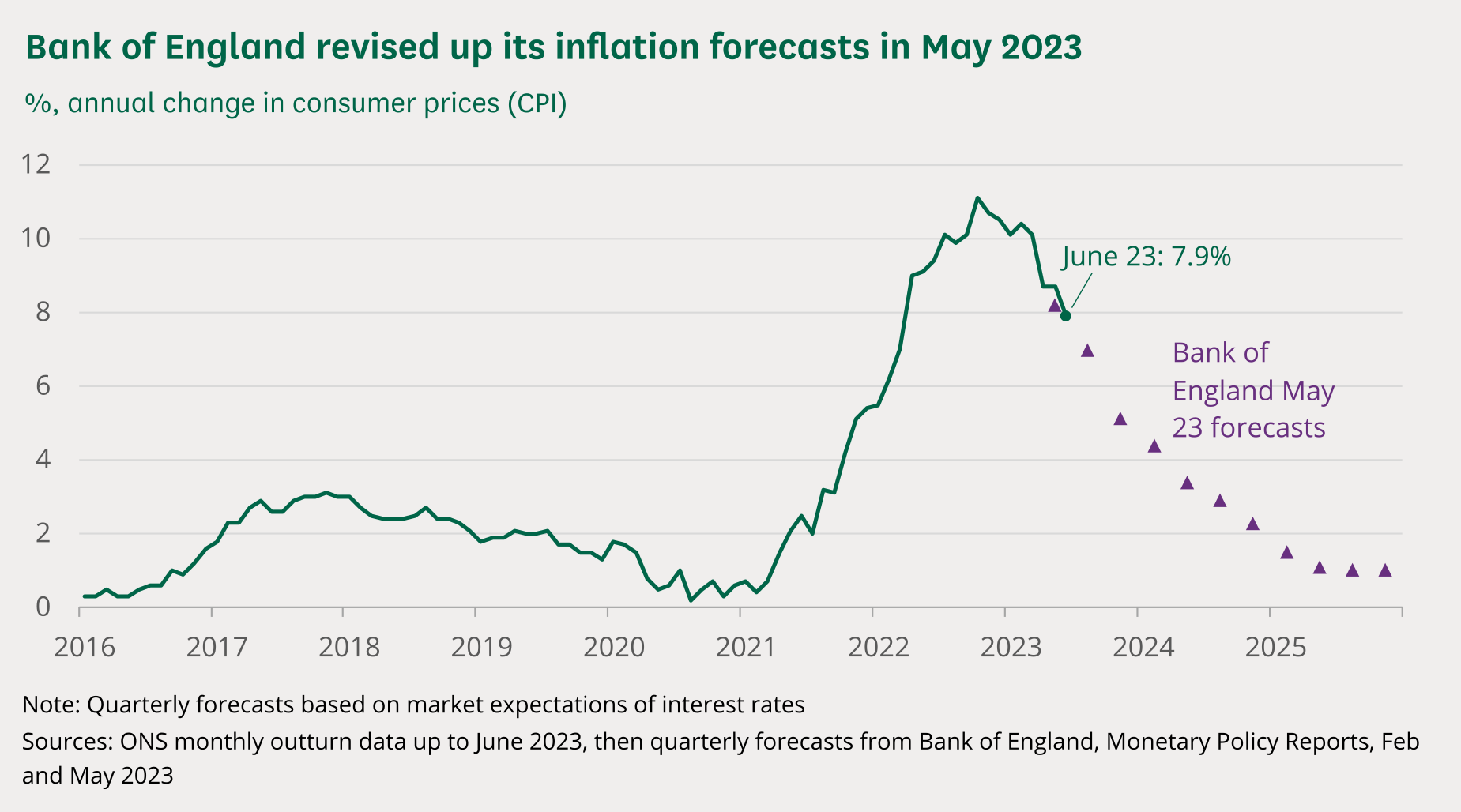

The United Kingdom, meanwhile, faces its own moment of decision. Inflation, which had eased earlier in the year, rose again in July to 3.8%, frustrating expectations of a smoother downward path. The Bank of England’s move to cut the base rate to 4.25% in May provided some temporary relief, but recent data have reinforced a more cautious tone within the Monetary Policy Committee. Attention now turns to the Autumn Budget, where the Treasury is expected to confront the delicate balance between maintaining market credibility and addressing cost-of-living pressures. Proposals under discussion, including a levy on banking sector reserves linked to quantitative easing, have already prompted considerable debate.

Across the Atlantic, the United States has presented a different balance of resilience and caution. Economic growth proved stronger than first reported in the second quarter, with gross domestic product expanding at an annualised rate above three per cent, suggesting domestic demand has been more durable than anticipated. Inflation has moderated gradually, though both headline and core measures remain above the Federal Reserve’s target. Labour market conditions have softened slightly, with unemployment moving above 4.0% and long-term joblessness creeping higher. The Federal Reserve left interest rates unchanged through the summer, maintaining its focus on the incoming data while continuing to reduce the size of its balance sheet. Markets responded positively, with major indices reaching new highs in late August, supported in particular by another season of robust technology earnings and ongoing enthusiasm for artificial intelligence. The outlook will hinge on whether disinflation can continue without undermining consumer spending, how the labour market evolves into the autumn and what guidance the Federal Reserve provides as policymakers weigh the timing of any eventual adjustment.

Major U.S. banks and investment firms have adjusted their year-end S&P 500 projections for 2025. Goldman Sachs raised its target to 6,900, Bank of America also increased its forecast to 6,666, driven by robust consumer spending and corporate earnings. Conversely, J.P. Morgan revised its outlook downward to 6,000, expressing caution due to ongoing trade tensions and potential economic headwinds.

As the final quarter of the year approaches, several themes appear central to the economic conversation. Japan must demonstrate whether its equity rally can be underpinned by domestic fundamentals. France and Germany need to navigate their respective fiscal and industrial difficulties if the eurozone is to regain momentum. The United Kingdom’s Budget will be scrutinised for the signals it sends about fiscal stability and the direction of policy into 2026. In the United States, the interaction of growth, inflation and central bank communications will remain a key driver of sentiment. These issues, together with the ongoing challenge of managing inflation and interest rates globally, will ensure that markets and policymakers alike remain alert through the closing months of the year.

Disclaimer: The author is an active, regulated Director and the founder of Moor Independent Financial Advisers Ltd. Moor IFA is a local, independent financial planning and investment management firm serving private clients and trustees. This guide is for information purposes and does not constitute financial advice, which should be based on your individual circumstances.

The value of investments may go down as well as up and you may get back less than you invest. Past performance is not a reliable indicator of future performance. This article is for information purposes and does not constitute financial advice, which should be based on your individual circumstances.

Jonathan Cotty, Chartered FCSI